Tabelle und Schaubilder zum Vergrößern anklicken.

Der DAX wurde am Freitag Tagesbester (grüner Pfeil) und schloss auf seinem 25. Rekordhoch in diesem Jahr! Im Wochenvergleich liegt der DAX ebenfalls vorn (grüner Pfeil). Gleichzeitig löste der DAX auch die Wiener Börse (ATX) von der Führungsposition seit Jahresbeginn (grüner Pfeil) ab.

Auf der Verlustseite stand das Texas-Öl in allen drei Zeitabschnitten (rote Pfeile) am Ende. Am Freitag fiel der Preis pro Barrel sogar unter die $45-Marke und testete damit den bisherigen Jahres-Tiefstand vom Januar.

An Wall Street endeten der Dow Jones und S&P 500 Index im Minus. Lediglich der Freiverkehrsmarkt (NASDAQ) weist noch im Plus seit Jahresbeginn auf.

Die zweite März-Woche stellte somit ein wahres Kontrastprogramm dar.

Der Euro fiel auf einen 12-jährigen Tiefstand (blauer Pfeil) und hat noch nicht seinen Boden gefunden. Bei der momentanen Konstellation ist bereits in diesem Jahr sogar ein Wechselkurs von 1 zu 1 möglich! Diese Prognose hätte ich noch vor drei Monaten ausgeschlossen. Das Zins-Differential zwischen den USA und Europa macht US-Anleihen attraktiver.

weiterer Text folgt

.png)

Text folgt

Text folgt

Retail sales dropped in February but gasoline prices are not to blame-rather auto sales. Retail sales in February declined 0.6 percent after decreasing 0.8 percent in January. As expected auto sales dropped 2.5 percent, following a 0.5 percent rise in January. Excluding autos, sales decreased 0.1 percent, following a 1.1 percent drop in January. Gasoline sales actually partially rebounded 1.5 percent in February after dropping 9.8 percent the month before. Excluding both autos and gasoline sales fell 0.2 percent after slipping 0.1 percent in January.

Some components may have been weak due to winter weather and a stay at home attitude.

Gains were seen in food & beverage, sporting goods & etc. and nonstore retailers (largely Internet sales).

The latest consumer sector numbers are curious. Confidence is still moderately high, discretionary income is moderately high, but spending is sluggish. Today's numbers will nudge down estimates for first quarter GDP growth.

There appears to have been a bubble in consumer spirits late into last year and early into this one, that is a brief surge that came and went and never materialized into a rise for consumer spending. The first read on consumer sentiment this month fell very sharply to 91.2, down 4.2 points from final February for the lowest reading since November. Sentiment peaked at 98.2 in mid-month January (green arrow) which was the highest reading in 8 years.

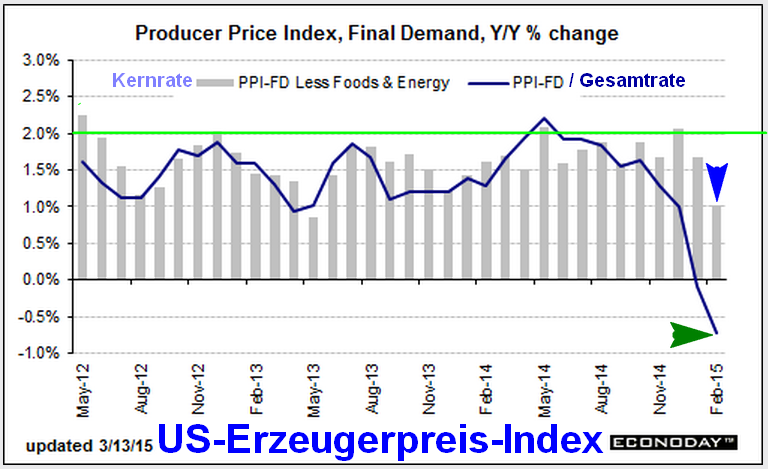

On a seasonally adjusted year-ago basis, PPI final demand was down 0.7 percent, compared to down 0.1 percent in January. Excluding food & energy, the PPI final demand was up 1.0 percent versus 1.7 percent the month before. Excluding food, energy, and trade services PPI inflation slowed to 0.7 percent on a year-ago basis, compared to 0.9 percent in January.

Inflation at the producer level remains essentially nonexistent. So far inflation numbers for February let the Fed stay loose on monetary policy.

.png)

Text folgt

Der Frühling kommt!

Heiko Thieme